Europe’s First Live AI Agent Payment

Source: The Rise of FintechDevCons (and an Agentic Commerce update), by Jas Shah

In early July 2026, a quiet but important milestone occurred in European fintech. CaixaBank, Spain’s leading bank with more than 12 million cardholders, completed the first real-world payment initiated by an artificial intelligence agent on behalf of a human cardholder.

This was not a lab experiment or simulated demo. It was a live transaction on standard merchant systems, secured by the same tokenization, identity verification, and real-time fraud monitoring that protect ordinary Visa payments today. The announcement, made on 2 July 2026, came just as Visa revealed at its Payments Forum in Paris that AI agents were already conducting live purchases across multiple European merchants, backed by more than 30 issuers.

For executives in European financial services, this is more than a technical curiosity. It signals that agentic commerce (where AI agents research, decide, and transact autonomously on behalf of users) has moved from prediction to production reality on the continent’s most trusted payment rails.

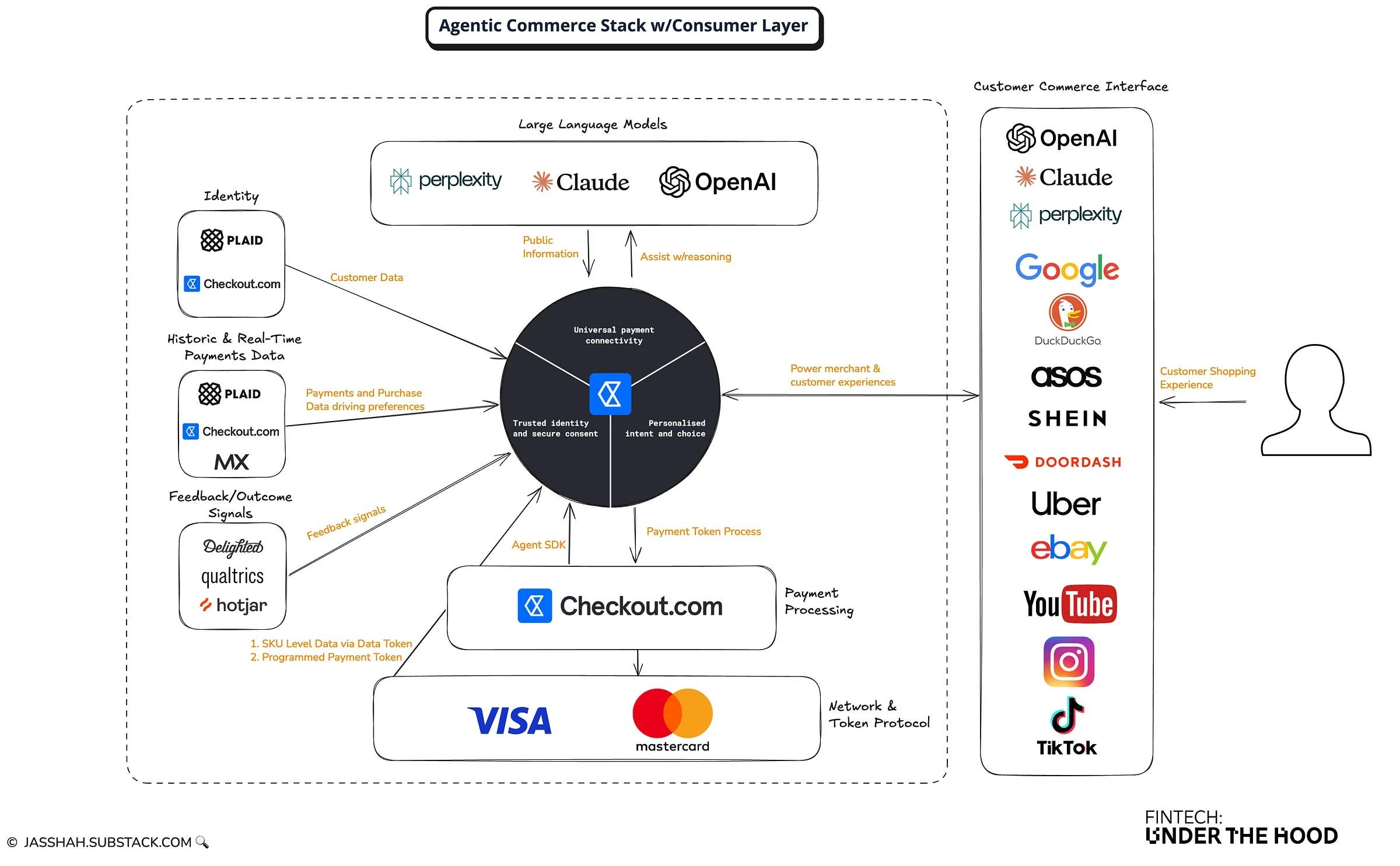

The Long Road to Agentic Commerce

Commerce has evolved in clear waves: face-to-face, then e-commerce, then mobile. Each shift required new infrastructure, new security models, and new consumer behaviors. Agentic commerce represents the next leap.

Visa articulated this trajectory clearly in its late-2025 predictions for 2026:

“We have moved from face-to-face commerce, to eCommerce, to mobile commerce, and now on to agentic commerce where agents transact on behalf of consumers and businesses. In 2026, AI-supported shopping will become very real for all of us, and agentic commerce will naturally follow.”

Source: Visa, “The Top Payments Predictions That Will Reshape 2026”, December 2025

The enabling technologies have matured rapidly. Large language models can now handle complex reasoning and multi-step tasks. Tokenization and modern authentication (such as Visa Payment Passkeys) allow secure delegation of credentials. Fraud systems have become sophisticated enough to monitor agent behavior in real time. What was missing was proof that these pieces could work together seamlessly on live European infrastructure while satisfying Strong Customer Authentication (SCA) requirements.

CaixaBank’s transaction supplied that proof.

CaixaBank’s Strategic AI Ambition

CaixaBank did not stumble into this milestone. It has been systematically building AI capabilities for years. In February 2025, the bank launched its “Cosmos” plan — a €5 billion investment in technology and processes running through 2027 as the core of its strategic roadmap.

The plan treats generative AI and cloud computing as transversal levers to drive operational excellence, personalize customer experiences, and embed new capabilities across the organization. CaixaBank established a dedicated Artificial Intelligence Office in late 2025 to oversee governance, compliance, and responsible deployment. It has already rolled out conversational AI agents for digital onboarding across approximately 40 retail products.

This latest pilot fits squarely inside that strategy. By proving that AI agents can initiate payments securely on existing rails, CaixaBank is positioning itself not merely as a user of AI but as an enabler of the next generation of customer interactions.

The Breakthrough: A Real Transaction on Existing Rails

According to CaixaBank’s official announcement:

“The transaction, carried out using real card data and existing merchant systems, confirms the viability of payments initiated by AI agents within the current infrastructure. The initiative forms part of the development of agentic commerce in Europe and supports progress towards new customer relationship models based on security, control and regulatory compliance.”

Source: CaixaBank Official Announcement, 2 July 2026

The technical details are deliberately reassuring for risk-averse institutions. The payment ran through Visa Intelligent Commerce, leveraging:

Tokenization to protect card credentials

Identity verification systems

Real-time fraud monitoring

Visa Payment Passkeys for biometric-backed authentication that supports SCA compliance

No new payment rails were required. The AI agent assisted with information gathering, option comparison, and decision-making, then initiated the transaction only under user-defined authorization parameters, with issuer oversight maintained throughout.

FinTech Futures, which broke the story in English-language trade media, summarized the significance:

“The pilot between CaixaBank and Visa tested the technical feasibility of AI agents making card transactions using existing payment infrastructure… proving the viability of payments initiated by AI agents within the current infrastructure.”

Source: Tyler Pathe, “CaixaBank completes first agentic payment with Visa”, FinTech Futures, 5–6 July 2026

Part of a Larger European Wave

CaixaBank’s achievement did not occur in isolation. On the same day (2 July 2026), Visa announced at its Paris Payments Forum that AI agents were already executing live transactions at independent European merchants including lastminute.com, Frasers, Cleverbridge, and BrickDepot. More than 30 issuers — ranging from Barclays, HSBC UK, BBVA, ING, Commerzbank, and Nordea to fintechs such as Revolut and Klarna — participated in the initial wave.

Mastercard moved in parallel, completing its own first agentic transaction in France around the same period with Crédit Agricole and Worldline. The competitive dynamic between the two networks is accelerating infrastructure readiness across the continent.

What This Means for the Future

For banks and fintechs Early movers gain a first-mover advantage in shaping how customers delegate financial tasks. Institutions that build robust agent orchestration layers, clear consent frameworks, and sophisticated agent-monitoring tools will be better positioned to capture volume and defend against disintermediation. Those that treat this as “just another channel” risk falling behind on both experience and risk management.

For payments infrastructure and networks The success of existing rails is the most important takeaway. Visa and Mastercard are demonstrating that their core strengths — tokenization, authentication, and fraud intelligence — translate directly to the agentic world. New capabilities such as Trusted Agent Protocols and Agentic Directories are emerging to solve identity and trust at scale. Banks that partner deeply with these networks will move faster than those attempting to build proprietary solutions.

For consumers and commerce Agentic experiences promise convenience but raise new questions about control, transparency, and error correction. Merchants will need to optimize sites and data for agent crawlers while implementing new bot-whitelisting and verification mechanisms. The winners will be those who make their offerings discoverable and trustworthy to verified agents.

Regulatory, risk, and trust challenges Europe’s regulatory environment is both an enabler and a constraint. Strong Customer Authentication rules are being satisfied today through Passkeys and issuer oversight, but liability frameworks for agent errors, fraudulent agent behavior, or disputed transactions remain underdeveloped. The EU AI Act will classify certain financial AI systems as high-risk, requiring transparency, human oversight, and robustness measures. Data protection rules (GDPR) and upcoming open finance initiatives (FIDA) will also shape how much context agents can access.

These are the next set of engineering and policy problems the industry must solve.

Europe’s opportunity Europe has a chance to lead globally in responsible agentic commerce. High digital payments penetration, sophisticated fraud infrastructure, and a maturing regulatory framework for AI and data give the continent an advantage over less regulated markets. The coexistence of private innovation (like this Visa-powered pilot) and public infrastructure thinking (the digital euro project) creates a uniquely European path: one that prioritizes both innovation speed and consumer protection.

Key Takeaways

CaixaBank’s milestone is best understood not as an isolated event but as the first public validation that agentic payments work on European rails today. For bank and fintech executives, the strategic questions are now urgent:

How quickly should we enable agent-initiated transactions on our cards and accounts?

What new risk, fraud, and consent models do we need to build or buy?

Which partnerships (networks, agent platforms, identity providers) will give us the fastest and safest path to market?

How do we govern these systems responsibly while remaining competitive?

The infrastructure is ready. The regulatory conversation is beginning. The competitive window is opening.

The institutions that treat agentic commerce as a core strategic priority — rather than a future curiosity — will define the next decade of European financial services. CaixaBank has taken the first visible step. The race is now on.