European Fintech Private Market Outlook 2026: The Year of Industrialisation

If the early 2020s were defined by experimentation and "growth at all costs," 2026 will be defined by industrialization. The European fintech ecosystem has pulled-through the correction of the last two years and matured into a disciplined, infrastructure-heavy marketplace.

Data from 2025 confirms that the freeze is over. Mergers and acquisition (M&A) activity is growing, a growing number of companies are orienting toward an IPO exit. Capital is flowing, but the rules of engagement have fundamentally changed. The year ahead will be characterized by a "flight to quality," where strategic consolidation and regulatory integration will disaplace a lot of the more speculative bets in recent history.

Here is the outlook for 2026:

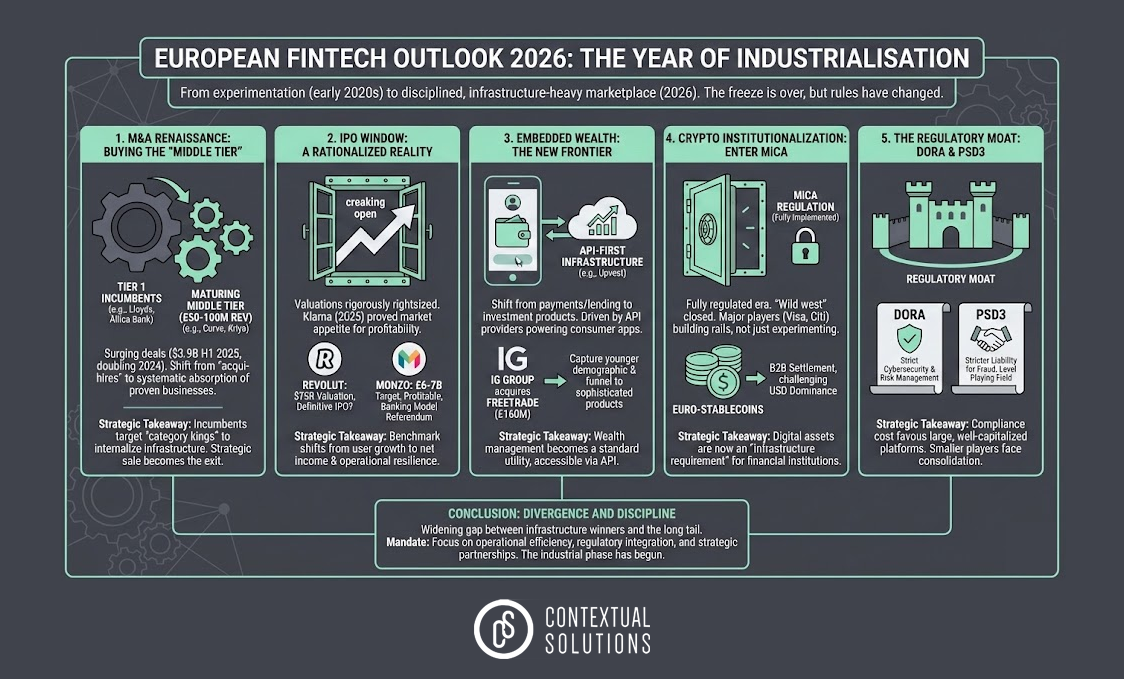

The Renaissance of "Middle Tier" M&A

The most immediate signal of market health is the resurgence of deal-making. In the first half of 2025 alone, deal values for transactions exceeding $100 million reached $3.9 billion, nearly doubling the total for the entirety of 2024.

However, the nature of these deals has shifted. We are moving away from opportunistic "acqui-hires" toward the systematic absorption of the "maturing middle tier." These are fintechs generating between £50 million and £100 million in revenue—proven businesses that have successfully navigated the startup phase but lack the hyper-growth velocity to stand alone in public markets.

The Return of the Strategic Incumbent

Perhaps the most critical trend for 2026 is the aggressive return of Tier 1 financial institutions as buyers. The "build vs. buy" debate has largely been settled in favor of "buy and integrate."

Lloyds Banking Group & Curve: The acquisition of Curve by Lloyds for approximately £120 million was a watershed moment. It signaled that incumbents are willing to pay for advanced digital interfaces to modernize their legacy stacks and defend against challenger banks.

Allica Bank & Kriya: In the B2B space, Allica Bank’s acquisition of Kriya (formerly MarketFinance) created a vertically integrated commercial lending powerhouse, aiming to deploy £1 billion in working capital to SMEs.

In 2026, expect incumbents to target "category kings" in specific verticals (payments, lending, and wealth) to internalize critical infrastructure. If you are a fintech in this "middle tier," the exit strategy is now likely a strategic sale rather than an IPO.

The Rational Reality of Public Markets

After a prolonged drought, the IPO market is finally reopening, but valuations have been rigorously rightsized. The listing of Klarna on the NYSE in late 2025 served as the bellwether. While its valuation of ~$15 billion was a far cry from its 2021 peak, the successful float proved that public markets have an appetite for profitable, mature fintechs.

Looking to 2026, all eyes are on the heavyweights:

Revolut: Following a secondary share sale that cemented a $75 billion valuation, Revolut is poised for what could be the definitive fintech IPO of the decade.

Monzo: With profitability secured and a valuation target of £6-7 billion, Monzo’s potential 2026 listing will serve as a referendum on the long-term viability of the digital banking model.

The "unicorn" backlog will begin to clear in 2026, but only for those with robust unit economics. For managers, this means the benchmark for "IPO-readiness" has shifted from user growth to net income and operational resilience.

From Embedded Payments to Embedded Wealth

For years, "embedded finance" largely meant payments and lending. In 2026, the frontier shifts to Embedded Wealth. As inflation erodes cash savings and younger generations seek financial autonomy, platforms are racing to integrate investment products directly into their user journeys.

The growth is being driven not by consumer apps building their own trading engines, but by API-first infrastructure providers. Upvest, a Berlin-based infrastructure provider, has become the backbone of this trend, powering investment products for neobanks like Zopa and established brokers like IG Group.

IG Group’s Acquisition of Freetrade: This £160 million deal exemplifies the trend. IG Group bought Freetrade not just for its technology, but to capture a younger demographic of mass-market investors, creating a funnel to move them toward more sophisticated products.

If your platform has a captive audience and a stored value balance, you will likely face pressure to offer investment products. In 2026, wealth management becomes a standard utility, accessible via API.

The Institutionalization of Crypto

2026 marks "Day One" of the fully regulated digital asset era in Europe. With the full implementation of the Markets in Crypto-Assets (MiCA) regulation, the "wild west" is officially closed.

This regulatory clarity has unlocked institutional participation. Major financial players are no longer experimenting in sandboxes; they are building rails.

The Stablecoin Pivot: The strategic investment by Visa and Citi into BVNK (a stablecoin infrastructure platform) confirms that stablecoins are now viewed as legitimate payment rails for global settlement, rather than just tools for crypto trading.

Euro-Stablecoins: MiCA provides a specific advantage for Euro-denominated tokens. We expect 2026 to be the year where Euro-stablecoins begin to challenge USD dominance for intra-European B2B settlement.

For European financial institutions, digital assets are no longer an eccentric reputational risk but an increasingly important component of core infrastructure. Expect banks to launch or partner on tokenized deposit and stablecoin initiatives to improve treasury management efficiency.

The Regulatory Moat: DORA and PSD3

Finally, the operating environment of 2026 will be defined by a "Regulatory Super-Cycle."

DORA (Digital Operational Resilience Act): Now fully enforceable, DORA mandates strict cybersecurity standards and third-party risk management. This has created a high barrier to entry for B2B fintechs; if you cannot prove DORA compliance, you cannot sell to a bank.

PSD3 (Payment Services Directive 3): The upcoming Third Payment Services Directive will further level the playing field for non-bank PSPs but introduces stricter liability for fraud.

Regulation has become a competitive moat. The cost of compliance favors large, well-capitalized platforms and incumbents. Smaller players who cannot afford the compliance overhead (or find creative ways to manage it efficiently) will likely be forced into consolidation.

Conclusion: Divergence and Discipline

The European fintech market in 2026 is structurally sounder than the exuberant market of 2021. It is a market defined by divergence: a widening gap between the infrastructure winners and the long tail of undifferentiated startups.

Focus on operational efficiency, regulatory integration, and strategic partnerships. The experimentation phase is over; the industrial phase has begun.