Europe's Quiet Rebalancing

For most of the past decade, the conventional wisdom about European technology went something like this: the continent builds clever companies, Americans buy them. Silicon Valley has the capital, the talent flywheel, and the appetite for audacity. Paris and Berlin have the regulators. Stockholm has the design sense. The rest is commentary.

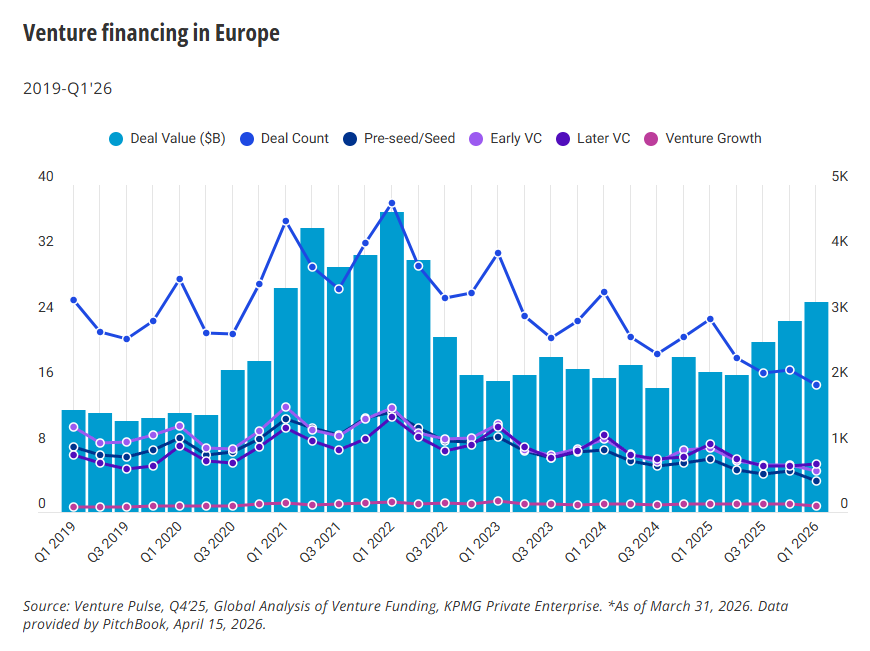

That story is getting harder to tell. In the first quarter of 2026, European startups raised $17.6 billion in venture funding, up nearly 30 percent year on year and marking the second consecutive quarter of growth after a long post-2022 stretch of caution, according to Crunchbase. It is the clearest signal yet that the continent's post-pandemic venture winter has ended, and it arrives alongside something more consequential: evidence that European fintech, after years of being measured against the United States and found wanting, has reached rough parity with American totals for the first time.

A market behaving like a grown-up

The Q1 figures reflect a market that is behaving less like a laggard and more like a mature venture ecosystem finding its own rhythm. Artificial intelligence claimed more than half of all European funding for the first time on record, a $9.2 billion wave that pulled in mega-rounds for Advanced Machine Intelligence, the Paris frontier lab founded by former Meta AI chief Yann LeCun, whose $1 billion seed became the largest in European history. Late-stage funding nearly doubled from a year earlier, reaching $9.2 billion across 83 deals, with capital flowing into AI hardware, autonomous systems, defence tech, and fintech. The other side of the ledger is equally telling. Overall deal volume fell by roughly 40 percent year on year, with seed activity down 44 percent. Capital is concentrating into bigger cheques for fewer companies.

Crunchbase's Gené Teare, who has been tracking the European market through its long cyclical slump, observed in her Q1 analysis that the quarter's totals were "well above the prior five quarters by funding amounts, signaling that European venture funding may be gaining momentum." That is a careful way of framing what the data increasingly suggests: the recovery is real, and it is being driven by the same forces reshaping venture globally rather than by any peculiarly European dynamic.

The geographic reshuffle

This pattern is global, not European. What makes it worth examining on this side of the Atlantic is that Europe is participating in the concentration trend on the winning side of it, not merely catching the fallout. The United Kingdom alone absorbed $7.4 billion of the quarter's total, with France at $2.9 billion and Germany flat at $1.9 billion. France has emerged as the continent's clear leader in frontier AI labs, hosting both Mistral and now Advanced Machine Intelligence. Germany's picture is more interesting than the flat headline suggests. Munich, driven by deep-tech and defence ventures, is displacing Berlin as the country's capital magnet, a meaningful reorientation for an economy that spent the 2010s building its startup identity around Berlin's consumer internet scene.

"We're seeing the early stages of a shift in Germany's VC investment landscape. While Berlin remains a strong hub for digital business models, particularly in fintech and consumer-facing B2C startups, capital is increasingly being allocated to deep-tech ventures. Munich is the first hub to benefit from this shift."

— Florian Merkel, Director of Tax and Head of Venture Services, KPMG in Germany

None of this would be especially novel had it happened in 2021. Concentrated capital, AI euphoria, outsize seed rounds: these are the familiar rhythms of a venture cycle. What makes the current moment genuinely different is the fintech story sitting underneath it, which points to something structural rather than cyclical.

The fintech parity moment

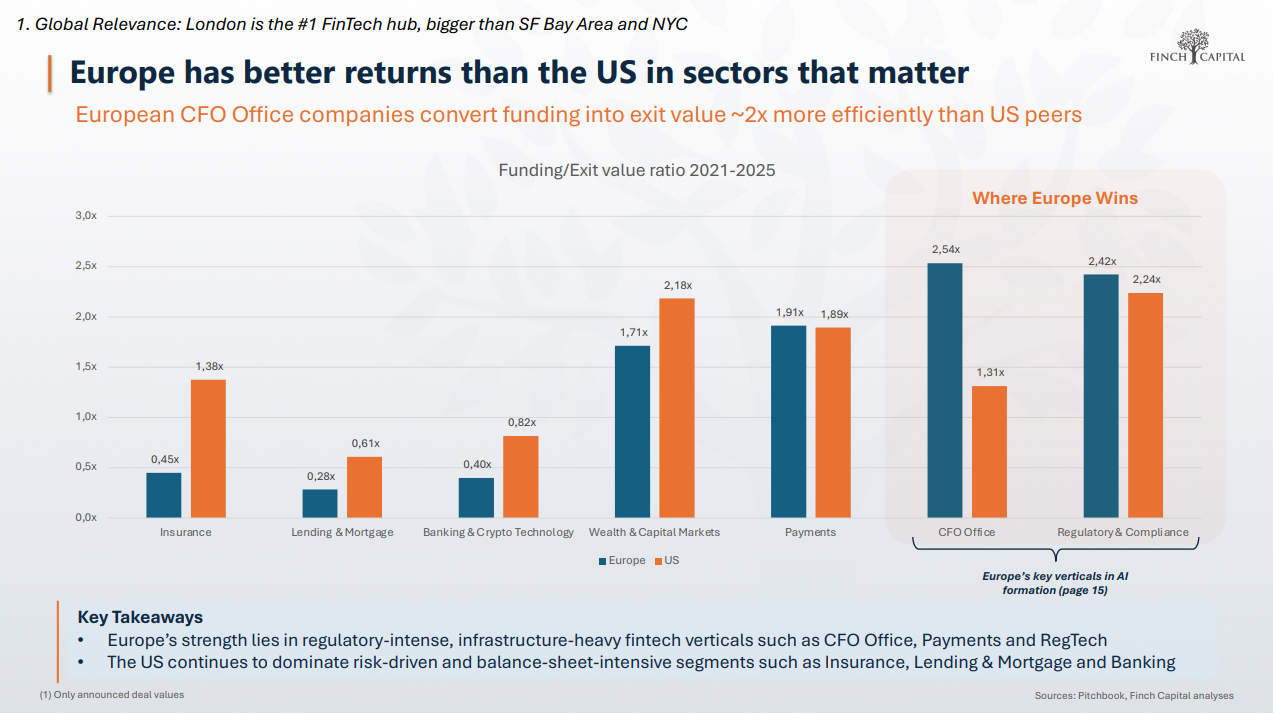

In March, the growth equity firm Finch Capital published its eleventh annual State of European FinTech report, and the headline finding was the sort of thing that tends to get filed under "surely not." Between 2022 and 2025, European fintech funding grew 37 percent while investment in the top U.S. hubs fell 13 percent, bringing both regions to rough parity at around €40 billion each over that four-year stretch. This is the first time European fintech has matched American fintech on capital raised, and it happened during a period when the prevailing narrative insisted Europe was slipping further behind.

"London's ranking as the world's number one FinTech hub is not symbolic. It reflects structural momentum. Europe has quietly built the deepest regulatory expertise and financial infrastructure talent pool globally. The funding gap with the US is narrowing, not because America is weakening, but because Europe is compounding."

Compounding is the operative word. The reversal did not happen because America suddenly forgot how to write software. It happened because Europe spent a decade building regulatory infrastructure that turned out to be a competitive asset. The UK's Financial Conduct Authority pioneered the regulatory sandbox model, which let fintechs test products under supervised conditions without the full weight of compliance. The EU's PSD2 directive forced incumbents across the bloc to expose customer data via APIs, allowing a generation of challengers to build on top of established banking infrastructure. The General Data Protection Regulation, much maligned when it arrived in 2018, established data norms that the rest of the world has gradually adopted. None of these were framed as industrial policy at the time. In aggregate, they produced a continent that is now unusually good at building regulated financial products, which happens to be where the enduring value in fintech sits.

Where Europe actually wins

The Q1 2026 data suggests the compounding is accelerating. Europe saw 273 fintech deals raising $3.7 billion in the quarter, with capital flowing into payments infrastructure, embedded finance, SME lending, and RegTech. Analysts at Finch Capital note that in capital-efficient, regulation-heavy segments such as CFO office software and compliance tools, European firms generated 2.54 times returns on invested capital between 2021 and 2025, roughly double the 1.31 times posted by American peers. The places where European fintech wins are the places where regulation and operational depth matter more than growth-at-any-cost. That is not a fashionable verdict in a market obsessed with frontier AI, but it is a durable one.

The sovereignty problem

There is a less flattering reading of the same data, and it deserves attention. Every European fintech round above €1 billion in the past five years has been led by American investors. Revolut, Klarna, and the continent's other marquee fintechs run on U.S. cloud infrastructure and U.S. payment rails. Finch Capital estimates that without American late-stage capital, Europe would face a €9 billion shortfall in the funding required to scale its breakout companies. European pension funds, according to the firm, allocate just 0.02 percent of their assets to venture capital, compared with 1.9 percent in the United States. Closing that gap could channel an estimated €37.5 billion annually into local ecosystems. That is a polite way of saying that Europe's sovereignty in financial technology is, at present, a leased apartment rather than an owned home.

"The €9bn dependency on US capital is real, but it's important to call it what it is: a policy gap, not a market verdict on Europe."

The distinction matters. The capital exists. The institutional willingness to deploy it domestically does not yet.

What executives should do with this

For European fintech executives, the strategic read is nuanced but broadly constructive. The concentration of capital at the top of the market rewards companies with defensible unit economics and genuine AI integration rather than broad survival-mode storytelling. The liquidity signal from bigger late-stage cheques should improve exit optionality for scale-ups weighing IPOs, secondaries, or strategic sales, particularly in a year when the global IPO window is widely expected to reopen. And the broader AI tailwind is genuinely European in a way previous technology cycles were not, with Paris, Munich, and London each pulling talent and capital into distinct specialisations. Boards that spent the past three years asking whether the recovery was real should now be asking whether their companies are positioned for the concentrated capital environment or still operating as if it were 2023.

The lesson Silicon Valley is still digesting

The deeper lesson is one that American founders and their investors are still absorbing. Regulation, long treated by Silicon Valley as a tax on innovation, turns out to be a genuine competitive asset when regulators know what they are doing. Europe's financial infrastructure talent was not built by accident. It was built by centuries of serving as an international financial centre, augmented by regulators who chose to be useful rather than merely punitive, and activated by founders who figured out how to navigate complexity rather than route around it. In a world where the next wave of fintech products must integrate with increasingly complex rules on AI, data, payments, and consumer protection, that competence compounds in ways that cheap capital and permissive regulation do not.

Whether Europe holds this position through the rest of the decade will depend on unglamorous things: pension reform, the willingness of European corporates to act as anchor investors in the way ASML did for Mistral, and the continent's ability to build late-stage capital pools that do not require a ticket on a transatlantic flight. Those are solvable problems. The harder one, which America now faces, is how to rebuild regulatory credibility and operational density in an industry where both increasingly determine who gets to build the next generation of financial infrastructure. On current evidence, Europe has a real head start, and for the first time in a long while, the continent's fintech sector is playing offence rather than defence.