Europe's Tokenized Markets Cannot Wait for Brussels

When thirty-nine of Europe's largest financial firms write the same letter on the same day, it is rarely because the regulatory weather is fine. On 21 April, a coalition that included Nasdaq, Boerse Stuttgart Group, Danske Bank, Union Investment, Germany's BVI fund association and more than a dozen national fintech federations sent a joint plea to Maria Luís Albuquerque, the European Commissioner for Financial Services, asking her to do something the Commission generally dislikes doing. They want her to break a flagship legislative package into pieces.

The package in question is the Market Integration and Supervision Package, or MISP, which the Commission proposed on 4 December 2025 as the centrepiece of its Savings and Investments Union strategy. The MISP is enormous. It rewrites parts of MiFIR, EMIR, the Central Securities Depositories Regulation, the Securitisation Regulation, MiCA, the ESMA Regulation and several other texts in a single sweep, while also moving direct supervision of significant trading venues, central counterparties and crypto-asset service providers to ESMA in Paris. Industry lawyers have already begun calling it the most consequential reopening of EU capital markets law in over a decade.

A Sandbox Few Wanted to Use

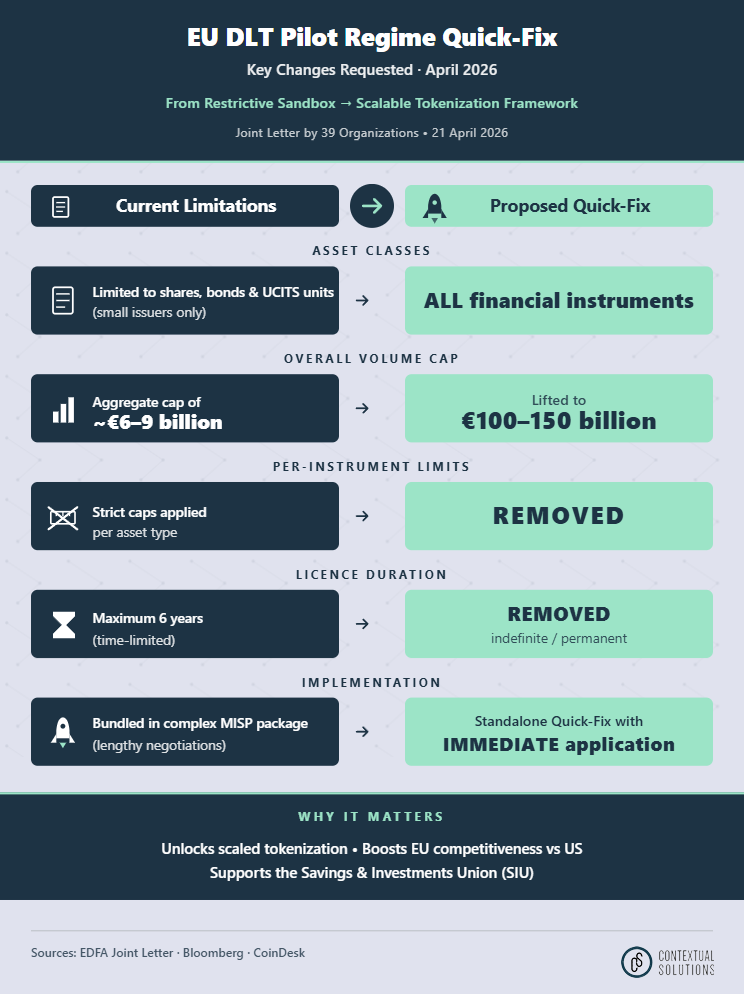

Buried inside this monumental file is a small set of amendments to something most Europeans have never heard of: the Distributed Ledger Technology Pilot Regime, or DLTPR. Live since March 2023, it is the EU's regulatory sandbox for tokenized securities. It permits a new category of trading venues, settlement systems and combined trading-and-settlement systems to operate on blockchain rails, with targeted exemptions from the rules built for paper-and-screen finance. In theory, it was supposed to make Europe the first jurisdiction where shares, bonds and fund units could be issued, traded and settled atomically on a distributed ledger under proper supervision. In practice, it has barely moved.

The numbers explain why this stopped feeling theoretical. In its June 2025 review, the European Securities and Markets Authority noted that only three DLT market infrastructures had been authorised in two years: CSD Prague, 21X AG and 360X AG. Trading volumes were minimal. ESMA itself concluded that asset eligibility was too restrictive, that thresholds were too low and that the six-year licence horizon discouraged the kind of long-term capital required to build market infrastructure. As OMFIF summarised the problem, market participants would not invest in DLT platforms when the regime capped aggregate volumes at around six billion euros and licences ran out in 2026 with no guarantee of renewal. The economics did not work.

Hostage to a Bigger File

The Commission's December proposal acknowledged most of this. As Ledger Insights summarised the substantive amendments, it raises the aggregate cap from six billion to one hundred billion euros, removes the rule limiting tokenized stocks to issuers worth less than five hundred million, opens eligibility to a wider range of MiFID II securities and lets crypto-asset service providers run DLT trading and settlement systems. It is, in other words, broadly the reform industry asked for. The problem is procedural. Bundled inside an eighteen-file legislative package that touches almost every piece of EU capital markets law, the DLT amendments are now hostage to negotiations on supervisory centralisation, fund delegation rules, consolidated tape design and the politics of ESMA's expanded remit.

The irony is sharp, because Albuquerque herself has spoken about tokenization in foundational terms. As her own services recently summarised her December 2025 remarks:

“DLT and tokenisation may well become the new operating system of financial markets.”

A February letter from a smaller coalition of tokenization firms including Securitize and 21X had already warned that the package's structural inertia could delay effective application until 2030. The April letter is the larger, broader version of that warning.

Five Asks, One Quick-Fix

Five concrete demands sit at the heart of the new letter. The signatories want the eligibility restriction on asset classes removed entirely so that all financial instruments can be tokenized under the regime, the volume cap lifted to between one hundred and one hundred and fifty billion euros, per-instrument limits deleted, the time limitation on licences scrapped and the law to apply immediately on entry into force without a transition period. None of these are radical. They are, in essence, the existing Commission proposal stripped of its bundling and put on a faster legislative track.

The American Shadow

The geopolitical subtext is what gives the request its weight. The letter is unusually direct on this point, warning that the United States and the SEC are actively moving capital markets on chain. Bloomberg's coverage and CoinDesk's reporting both led with the same framing. America is moving. Europe is drafting. The Genius Act for stablecoins is law. Major US banks and asset managers are already running tokenized deposit and money-market-fund products at institutional scale. The fear in Frankfurt and Paris is not that Europe will lose a race for cryptocurrency speculation, which it never wanted to win, but that it will lose the standards battle for serious tokenized capital markets, which it has explicitly tried to lead.

The Infrastructure Is Already Going In

The letter does not arrive in isolation. Six days earlier, on 15 April, SIX Group put equities data from its Swiss and Spanish exchanges, representing more than two trillion euros in combined market capitalisation, on-chain through Chainlink's DataLink service, opening that data to over twenty-six hundred applications across more than seventy-five blockchain networks. The same day, the ECB's Piero Cipollone delivered a keynote at Harvard describing tokenization as a potential general-purpose technology and laying out the Eurosystem's Pontes and Appia projects, which are intended to deliver wholesale central bank money settlement on DLT in the third quarter of 2026 and a full blueprint for an integrated European tokenized financial ecosystem by 2028. As Cipollone put it when launching the roadmap:

“Appia is about building a road from today's financial system to tomorrow's tokenised markets, firmly grounded in central bank money.”

The infrastructure is being built. The data is being plumbed. The settlement layer has a date on it. The legal regime that is supposed to govern all of this is sitting in a Brussels in-tray.

Coherence and Its Costs

The Commission's response so far has been characteristically institutional. As CoinDesk noted, the Commission prefers to pass the full package together, viewing coherence between supervision, market structure and DLT as a feature rather than a constraint. There is something to be said for that view. Carving out individual files invites others to demand the same treatment, and the MISP's internal logic depends on the supervisory architecture and the substantive rules moving in step.

Coherence has costs, though, and in fast-moving technology markets those costs compound. The DLTPR Quick-Fix is a test of whether European financial regulation can distinguish between the changes that need a grand bargain and the ones that need a green light. By summer, the answer will tell investors, banks and infrastructure operators a great deal about whether Europe intends to write the rulebook for tokenized markets, or read someone else's. France FinTech, in its statement of support, put the question with characteristic French directness:

“Launching a DLTPR Quick-Fix would send a strong signal: that of a Europe capable of combining regulatory ambition and agility.”

Without that signal, the alternative is continued drift, with capital and innovation moving steadily across the Atlantic while the file works its way through committee.