Europe Just Laid the Foundation for Its Tokenised Financial Future

For years, the phrase "tokenised capital markets" lived in the awkward space between proof-of-concept and production. Central bankers name-checked distributed ledger technology in speeches, fintech firms built prototypes, and a handful of sovereign issuers dipped their toes into digital bonds. It was all promising enough to warrant attention but tentative enough to justify inaction. That era, at least in Europe, appears to be over.

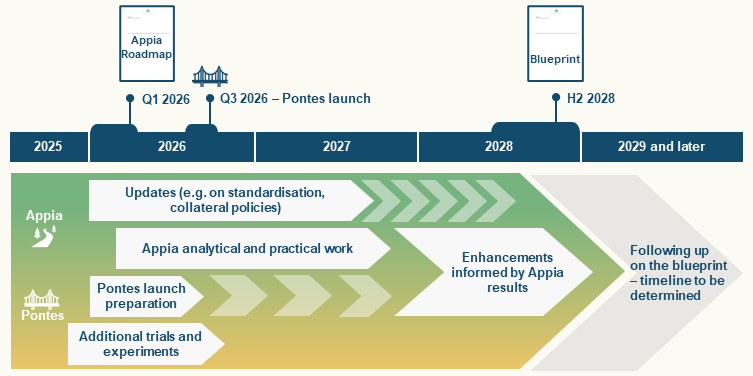

On 11 March, the Eurosystem published the roadmap for Appia, a strategic initiative designed to shape the development of a European tokenised wholesale financial ecosystem anchored in central bank money. It is not a pilot programme. It is not a sandbox exercise. It is the institutional blueprint for what the European Central Bank hopes will become the plumbing of tomorrow's capital markets, and it comes with a timeline, a set of design principles, and a public consultation deadline of 22 April 2026.

"With Appia, we are building a road from today's financial system to tomorrow's tokenised markets, firmly grounded in central bank money."

Piero Cipollone, Member of the Executive Board, ECB - Official ECB press release, 11 March 2026

The ambition is considerable, but it does not arrive out of thin air. Since 2021, European issuers have placed close to €4 billion in DLT-based fixed-income instruments, a figure that includes the first digital sovereign debt issuances by EU member states. The regulatory scaffolding has been erected in stages: MiCA established a unified framework for crypto-assets, and the EU's DLT Pilot Regime gave market participants a controlled environment in which to test tokenised securities within existing legal structures. By the time the ECB conducted its 2024 exploratory work on wholesale settlement technologies, the exercise drew 64 participants from across nine jurisdictions, who between them ran more than 50 trials and experiments processing roughly €1.6 billion in transactions.

That scale of participation told the Eurosystem something important: demand for programmable assets, atomic settlement, and round-the-clock operations was not hypothetical. It was real, specific, and growing.

The twin obstacles

Two structural problems, though, kept threatening to strangle progress. The first was platform fragmentation. Across Europe, a patchwork of competing DLT networks had emerged, each with its own protocols, standards, and governance. This sliced liquidity into narrow pools, inflated integration costs for participants who wanted to operate across platforms, and created precisely the kind of balkanised landscape that Europe's capital markets have struggled with for decades in their traditional form.

The second problem was the absence of a trusted on-chain settlement anchor. Without one, market participants remained wary of settling wholesale transactions in private tokens whose value could fluctuate or whose issuers carried credit risk. A buyer of a tokenised bond does not want to receive payment in an asset that might lose value before the trade clears. This is not an abstract concern; it is the reason that central bank money has historically served as the bedrock of large-value settlement, and nothing in the shift to digital rails changed that fundamental requirement.

Without addressing both issues, Europe risked watching its fragmented digital infrastructure fall further behind international competitors, or worse, becoming dependent on foreign-built platforms for a core piece of financial sovereignty. The stakes, as Cipollone framed them in his 23 March keynote, are considerable.

"The potential of tokenisation for Europe is significant: more efficient and more innovative financial markets, and the prospect of genuine cross-border integration that has long eluded Europe's fragmented capital markets."

Piero Cipollone, Member of the Executive Board, ECB - Keynote speech, 23 March 2026

The Appia and Pontes strategy

The Eurosystem's response is a two-track strategy, though officials are quick to stress that the two tracks share a single destination. As Fiona van Echelpoel, Deputy Director General at the ECB, explained at a focus session on the Appia roadmap:

"That inspired us to launch two workstreams under a single programme -- Pontes and Appia, the bridge and the road."

The near-term track, Pontes, is a DLT bridge that will connect market platforms directly to the Eurosystem's TARGET Services, the existing settlement infrastructure for euro-denominated transactions. Pontes is scheduled to launch by the end of the third quarter of 2026, with user testing expected to begin as early as August. Its purpose is immediate and practical: it allows market participants to settle tokenised wholesale transactions in central bank money right away, providing the trusted settlement anchor the market has been asking for.

Appia is the longer arc. As Cipollone explained in his Brussels keynote:

"Appia sets out the longer-term vision for a European tokenised financial ecosystem. Through a combination of analytical and practical work, it aims to deliver a blueprint by 2028 in cooperation with all relevant stakeholders."

Piero Cipollone, Member of the Executive Board, ECB - Keynote speech, 23 March 2026

That blueprint will be developed through six interlocking building blocks. These cover asset interoperability and technical standards, the integration of monetary policy operations and collateral management onto DLT, the design of European tokenised central bank money infrastructure (including the question of whether the ecosystem should centre on a single shared network or multiple interconnected ones), the international dimension and its implications for euro relevance, safety and resilience requirements, and the overall implementation strategy.

The design principles the Eurosystem has articulated are notable for their specificity. Technological neutrality is the default, meaning the initiative is not picking favourites among DLT platforms, but European governance, common standards, contestability, and robustness are non-negotiable. The Eurosystem is also deliberately opening the process to the market, because as Cipollone emphasised, the central bank can lay the rails but cannot drive all the trains.

"The services, liquidity and business models that will make tokenised markets valuable must come from the market itself."

Piero Cipollone, Member of the Executive Board, ECB - Keynote speech, 23 March 2026

The public-private feedback loop

This collaborative ethos is not rhetorical. The 2024 exploratory trials directly shaped the technical design of Pontes. In January 2026, the ECB announced that DLT-based assets issued through central securities depositories would become eligible as Eurosystem collateral starting 30 March 2026, a decision that came as a direct response to market feedback about what tokenised markets needed in order to scale. The policy change is significant because collateral eligibility is one of the most powerful levers a central bank can pull; it shapes what assets institutions hold, how they manage liquidity, and which instruments attract investment. The speed of the transition from experiment to infrastructure has not gone unnoticed by industry participants.

"A year after testing, we have a short-term solution we can actually use. That's a speed of light for any central bank."

Meanwhile, the private sector has been moving in parallel, and the conversations between public and private actors are increasingly converging on the same priorities.

"Digital innovation is about using new technologies to improve services and to improve interconnection."

In early March, Clearstream, DTCC, and Euroclear, three of the world's largest financial market infrastructures, released a joint white paper with Boston Consulting Group proposing a framework for digital asset securities interoperability. The paper identified DLT network fragmentation as one of the most pressing barriers to adoption and proposed five foundational pillars, spanning ownership recognition, asset movement protocols, and compliance, to enable trusted interoperability at scale. The alignment between this private-sector initiative and the Eurosystem's Appia vision is difficult to miss; both identify the same core problem of fragmentation and arrive at complementary prescriptions centred on common standards.

What it means in practice

For financial services executives, the timeline is no longer abstract. Collateral rules changed on 30 March, meaning that DLT-issued assets can now be used in Eurosystem credit operations. Pontes is expected to reach production readiness within months. Product development teams, risk managers, and capital markets strategists need to factor in the implications of programmable assets, atomic delivery-versus-payment settlement, and the possibility that shared-ledger models will reshape post-trade infrastructure more fundamentally than anything since the move to T+2 settlement cycles.

"New technology gives us the opportunity to trade 24/7 and manage risk more effectively if the collateral rails are right."

That "if" in Woodward's statement is precisely what the Pontes launch and the Appia roadmap are designed to resolve. The international dimension also warrants attention. One of Appia's explicit objectives is to ensure the continued relevance of the euro as an international currency. If Europe builds a tokenised ecosystem that works, it will attract participation from beyond the EU's borders. If it does not, foreign infrastructure providers will fill the gap on their own terms. Cipollone's framing in his March keynote was pointed: Europe already succeeded in building a single currency, and now it has the chance to build a single digital financial market alongside it.

There is a tendency, when central banks announce strategic initiatives, to file them under "important but distant" and return to more pressing concerns. That would be a mistake here. The Appia consultation deadline falls on 22 April, and the feedback gathered will directly shape the analytical and practical work that follows. Expressions of interest to participate in the initiative's building blocks are being accepted now. The architecture of Europe's tokenised future is being drawn, and the institutions that engage with the process will have a meaningful say in how it looks. Those that wait may find the road already built when they arrive, with the on-ramps designed for someone else.