The 2026 German Fintech & Banking Market: How Europe’s Largest Economy Learned to Reward Resilience Over Hype

Our new report maps the forces reshaping German banking and financial technology in 2026, from agentic AI to record insolvencies.

For years, the received wisdom about German fintech went something like this: the market is enormous, the consumers are conservative, the regulators are slow, and the opportunity is perennially just around the corner. The latest edition of our Banking & Fintech Market report suggests that this framing has finally expired. In its place is a more interesting reality, one in which Germany’s famous caution has become a genuine competitive advantage, and the companies that survived the funding winter are now building something more durable than the venture-fueled neobanks of the early 2020s.

The headline numbers tell a contradictory story, as corporate insolvencies hit a decade-long high of nearly 24,000 cases in 2025, according to Creditreform, with estimated creditor losses of around €57 billion. The broader economy stagnated for a second consecutive year. And yet German fintechs and insurtechs reportedly secured approximately €14.2 billion in funding over the same period. The sector has decoupled from the macroeconomic malaise surrounding it.

The era of blitzscaling neobanks is definitively over. What has replaced it is a market that prizes two archetypes: the “Super-Specialist,” exemplified by companies like Pliant and Raisin that dominate narrow verticals with surgical precision, and the “Platform Titan,” a category now led by Trade Republic as it evolves from neo-brokerage into a full-service financial ecosystem.

The Trade Republic Phenomenon

No company better illustrates the new German fintech thesis than Trade Republic. The Berlin-based platform closed 2025 with a €1.2 billion secondary transaction that valued the firm at €12.5 billion, roughly double its 2022 valuation. Backers include Peter Thiel’s Founders Fund, Sequoia, Fidelity, and Singapore’s GIC. Crucially, no new primary capital was raised. Trade Republic has been profitable for three consecutive years and says it does not need fresh funding.

The company now serves more than 10 million customers across 17 European countries, with assets under management exceeding €150 billion. About 70 percent of its users are first-time investors, which speaks to its role in widening market participation at a time when European pension systems face growing demographic pressure. Germany’s planned pension reform, the Aktienrente, is expected to funnel millions of additional retail investors into capital markets, and Trade Republic’s infrastructure is positioned to absorb much of that demand.

N26: From Disruptor to Compliance Project

If Trade Republic represents the aspirational arc, N26 serves as the cautionary tale. Once valued at $9 billion, the company spent much of 2025 contending with regulatory containment by BaFin. A special audit revealed serious anti-money-laundering and governance deficiencies, resulting in a ban on new mortgage lending in the Netherlands, the re-installation of a special compliance monitor, and a valuation that has cratered to roughly $3 billion.

In December, N26’s supervisory board appointed Mike Dargan, a veteran UBS executive, as incoming CEO, effective April 2026. Both co-founders have stepped back from operational roles. The transition signals that N26’s path to a public listing is likely years away. The bank remains profitable on an interest-driven revenue model, but rebuilding regulatory credibility will take time.

The Great Cleanup

The divergence between Trade Republic and N26 reflects a broader sorting mechanism. The report describes 2025 as a year of “filtration,” in which capital concentrated around companies with defensible infrastructure and clear profitability paths. Companies that lacked these attributes faced forced consolidations, distressed acquisitions, and insolvencies.

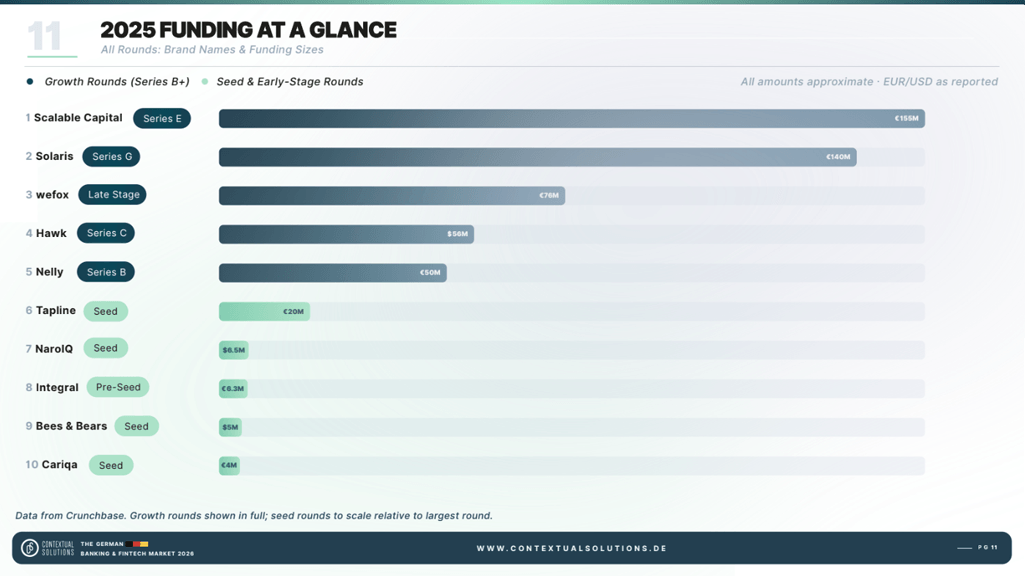

The most prominent casualty was Solaris, the banking-as-a-service platform once valued at $1.6 billion. Japan’s SBI Holdings acquired a majority stake of more than 70 percent as part of a €140 million round, ending Solaris’s run as an independent unicorn. Dock Financial, another BaaS intermediary, did not survive at all, entering insolvency proceedings mid-year.

The funding landscape took on a “barbell” shape: significant capital flowed to late-stage winners and promising early-stage AI and climate-finance startups, while the mid-market faced a squeeze. Scalable Capital raised €155 million in Series E funding; Hawk, a Munich-based AML technology provider, secured $56 million. Corporate venture arms from Commerzbank, Deutsche Börse, and Allianz X stepped in where traditional VC pulled back, suggesting a deepening integration between incumbents and the startups they once viewed as threats.

Regulation as Moat

Perhaps the most counterintuitive argument in the report is that Germany’s regulatory environment, long criticized as a barrier, has become its greatest structural asset. In a global landscape marked by instability and fraud, a BaFin seal of approval now commands a premium.

The 2026 regulatory calendar is dense. Crypto firms must obtain full MiCA licenses by July or cease EU operations. The EU AI Act’s high-risk provisions take effect in August, directly affecting fintechs using AI for credit scoring and insurance pricing. By November, member states must offer certified digital identity wallets under eIDAS 2.0, potentially transforming KYC onboarding across the continent. For traditional banks, the Basel III reforms and CRD VI governance rules add further compliance weight. The expected finalization of PSD3 promises to replace the existing open banking framework with improved API standards and fairer terms for non-bank payment providers.

The Agentic Frontier

The buzzword of 2026, according to the report, is “agentic.” The financial sector is moving beyond chatbots toward AI systems that execute complex workflows autonomously. Commerzbank has deployed a generative AI avatar called “Ava” to handle customer queries around the clock. LBBW’s internal tool “blue.gpt” has become a case study in compliant enterprise AI. The Sparkassen-Finanzgruppe, Germany’s vast savings bank network, is planning to roll out crypto trading to its 50 million customers via DekaBank.

The report anticipates autonomous AI agents capable of negotiating loan rates, managing liquidity, and executing trade strategies without human intervention. This is a significant conceptual leap from the pilot programs of recent years, raising questions about accountability and the evolving role of human advisors in a system increasingly run by algorithms.

What Comes Next

Germany’s consumer habits are shifting, too. Cash has fallen below 50 percent of point-of-sale volume for the first time. ETF savings plans surged 34 percent to 9.5 million in 2024, with annual savings volume reaching €22.7 billion in 2025. Crypto adoption hit 27.3 million users, about 33 percent penetration, though older demographics remain skeptical.

Looking further ahead, B2B embedded finance is displacing retail buy-now-pay-later as the growth frontier, with platforms like Banxware integrating financial layers into corporate procurement systems. The ECB’s digital euro project, targeting a 2029 issuance, is prompting German banks to build coexistence infrastructure. And the high insolvency rate, far from being purely destructive, is expected to release talent back into the ecosystem and produce a wave of second-time founders building leaner, compliance-first companies.

The overall picture is one of an ecosystem that has traded exuberance for discipline. Germany’s fintech sector is no longer trying to move fast and break things. It is trying to move deliberately and build things that last. For international observers accustomed to Silicon Valley’s tempo, the pace may seem glacial. For the companies that have survived the correction, it may turn out to be exactly right.