Europe's banks are consolidating again

A long-promised wave of mergers is finally arriving, and the contest for Commerzbank shows both its momentum and its limits.

The reawakening

“I’m pretty convinced that there will be fewer banks [by 2030]. There will be winners and losers and the dispersion between winners and losers will be much, much greater. Some will consolidate. Some will be wiped out.”

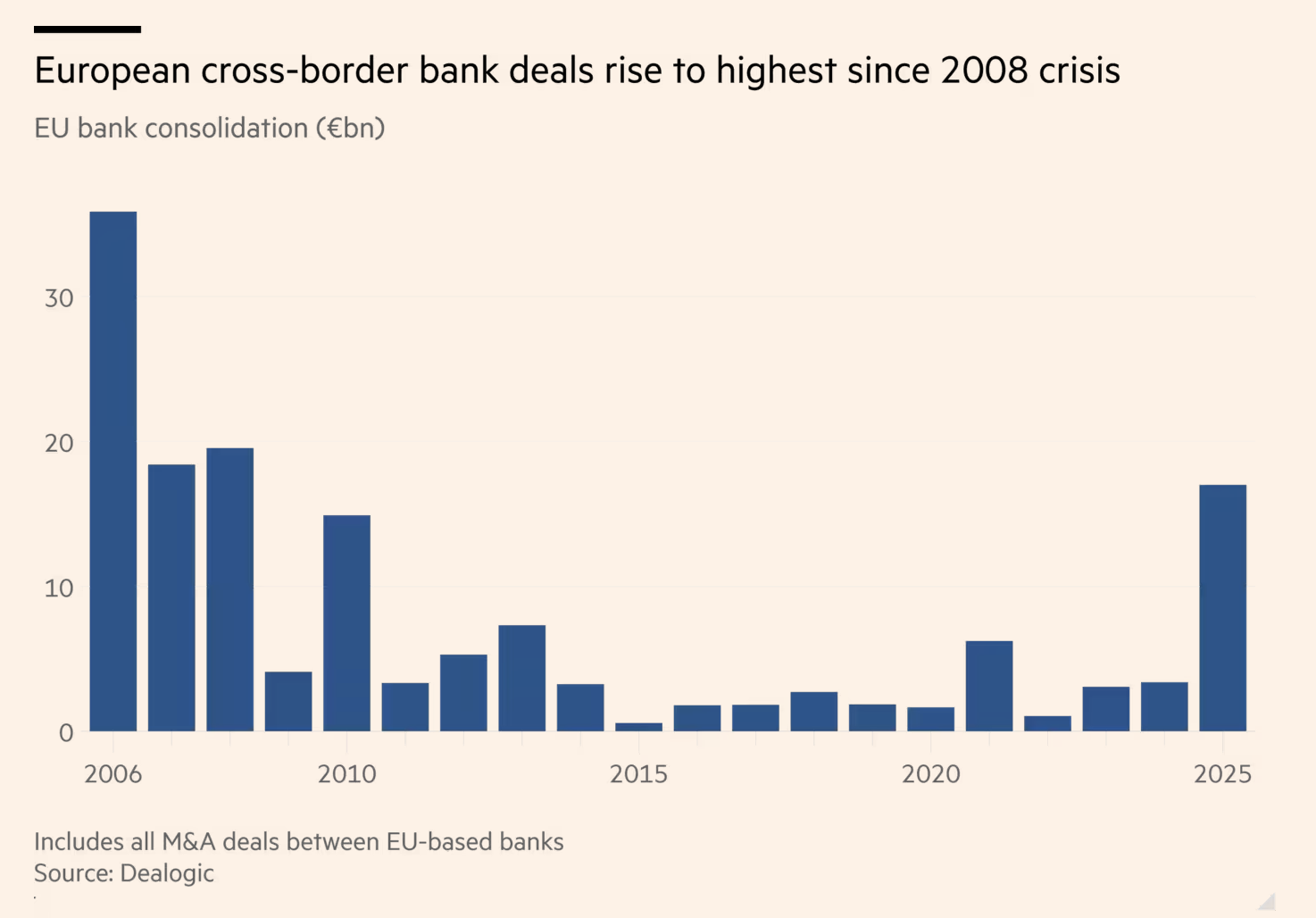

For most of the past decade, talk of consolidation among Europe's banks was a perennial that never quite bloomed. Low interest rates squeezed margins, regulators kept supervision fragmented along national lines, and governments treated their largest lenders as strategic assets to be defended rather than combined. That mood has lifted. 2025 was the strongest year for European bank mergers and acquisitions in more than a decade, and the momentum has carried firmly into 2026.

The most visible test of how far the appetite extends is unfolding in Frankfurt. UniCredit, Italy's second-largest bank, has spent more than a year building a position in Commerzbank, and in May it launched a voluntary exchange offer of 0.485 of its own shares for each Commerzbank share, valuing the German lender at roughly 35 billion euros. By 9 June the Italian bank's combined holding had risen to 37.68 percent, assembled from a direct stake of 26.77 percent plus shares tendered into the offer, with derivatives lifting its potential reach toward 54 percent. Commerzbank's board formally rejected the bid on 18 May, calling it inadequate and a distraction from its own growth plan, and has since dismissed the rising acceptance figures as misleading. The German government, which holds about 12 percent of the bank, continues to resist any loss of independence.

Andrea Orcel, who has made the pursuit the defining campaign of his tenure, has framed the offer less as a conventional takeover than as an invitation to negotiate.

"It is now time to talk."

The structure of the bid is revealing. Under German law a holding above 30 percent would normally trigger a mandatory full offer. UniCredit designed its move to clear that threshold while stopping short of control, giving it the freedom to buy further shares in the open market and to press its case without committing the capital a full acquisition would consume. The first acceptance phase closes on 16 June, with an extended window possible to 3 July.

Why now

The forces behind the revival are more economic than sentimental. Years of higher rates left banks with strong profits and thick capital buffers, and as rates ease, lenders face growing pressure to diversify income toward fees, wealth management and payments. Analysts estimate the sector is sitting on excess capital that could exceed 500 billion dollars over the coming years, money that increasingly funds acquisitions rather than share buybacks. Scale matters too for the heavy fixed costs of technology, from cloud migration to fraud detection and the early deployment of artificial intelligence, where larger institutions can spread the bill across a wider base of customers. Beneath all of this sits a competitive anxiety. European banks remain small by the standards of their American and Asian peers, and few executives believe a fragmented sector can fund the investment that global competition now demands.

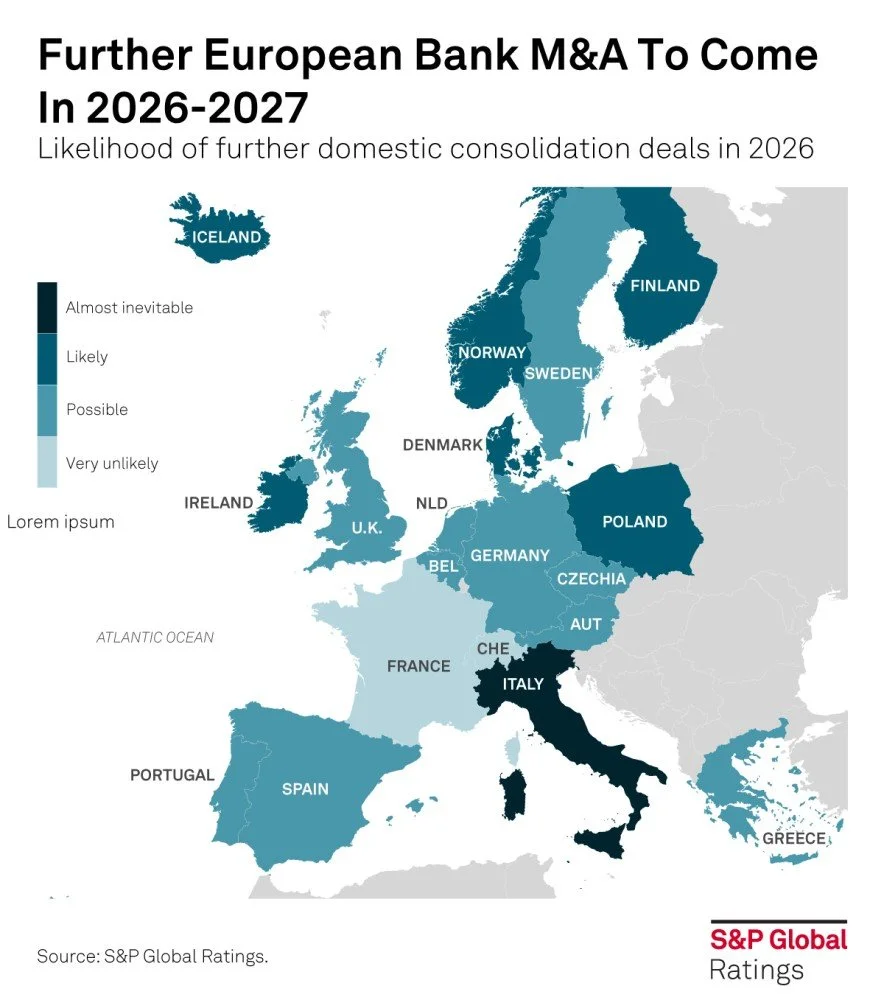

Consultants expect the trend to broaden. S&P Global Ratings anticipates further deals through 2026 and 2027, with Italy, the Nordics and Poland among the likely hotspots, while Oliver Wyman has argued that in-market consolidation will deepen as capital and policy align. The prevailing view on the advisory side is that the current activity marks an opening rather than a culmination.

"We have not yet seen the peak; 2026 and 2027 are expected to be busy bank M&A years."

The deal that worked

While the Commerzbank saga illustrates the obstacles to cross-border banking, another transaction shows what success looks like. In May 2025 Austria's Erste Group agreed to buy a 49 percent controlling stake in Santander Bank Polska, together with associated asset management interests, for around 7 billion euros. The deal closed in January 2026 after regulatory clearance, handing Erste control of Poland's third-largest bank, later rebranded under its own name, and deepening its footprint across central and eastern Europe. It ranks among the largest cross-border banking moves the continent has seen in years.

The comparison with Frankfurt is instructive. Poland's market is fast-growing and politically receptive to a regional consolidator, and the seller was a willing one. Erste gained scale in a dynamic economy without the public resistance that has met UniCredit in Germany. For executives weighing where to deploy capital, the lesson is that geography and political consent often shape outcomes more decisively than financial logic alone.

The politics of borders

Domestic mergers continue to face the fewest obstacles. Crédit Mutuel's German arm acquired Oldenburgische Landesbank, mid-sized lenders across Italy and Spain have combined, and Britain has seen a run of building-society tie-ups. Cross-border ambition is where resistance concentrates, because national governments still regard control of a large domestic bank as a question of sovereignty rather than of markets.

Brussels is trying to change that calculus. The European Union's push for a Savings and Investments Union, alongside long-standing efforts to complete the Banking Union through freer cross-border capital and liquidity flows and a common deposit-insurance scheme, is intended to make pan-European banking both possible and attractive. Digital-finance rules such as MiCA point in the same direction, since compliance favours institutions with the resources to absorb it. The political reality is that supervisory fragmentation and national intervention, both vividly on display in the Commerzbank fight, still raise the cost and uncertainty of any deal that crosses a border.

What comes next

The wave now building is unlikely to resemble the megamerger frenzy of the late 1990s. It is more strategic and, for the moment, more domestic, with cross-border activity advancing where political conditions allow it. Should it persist, the payoff could be considerable. Larger and more resilient lenders would be better placed to fund business investment, modernise their technology and stand against rivals whose home markets dwarf any single European one.

The risks are real as well. Cross-border integration is difficult to execute across different cultures, systems and regulators. Over-consolidation could thin competition in some domestic markets, and branch rationalisation will test customers and small businesses alike. Whether the benefits materialise depends heavily on whether Europe's policymakers deliver the simplifications they have promised.

For now, the outcome in Frankfurt will set the tone. If UniCredit can turn a sizeable minority position into genuine influence over Commerzbank without provoking a political backlash that deters others, the rest of the continent's bankers will take note. If it stalls, the message will be that Europe still wants national champions but not the cross-border mergers that would create them. Either way, 2026 and 2027 look set to be the years in which the long-deferred reshaping of European banking is finally tested in practice.