Europe's Quiet Push to Rewire Its Financial System

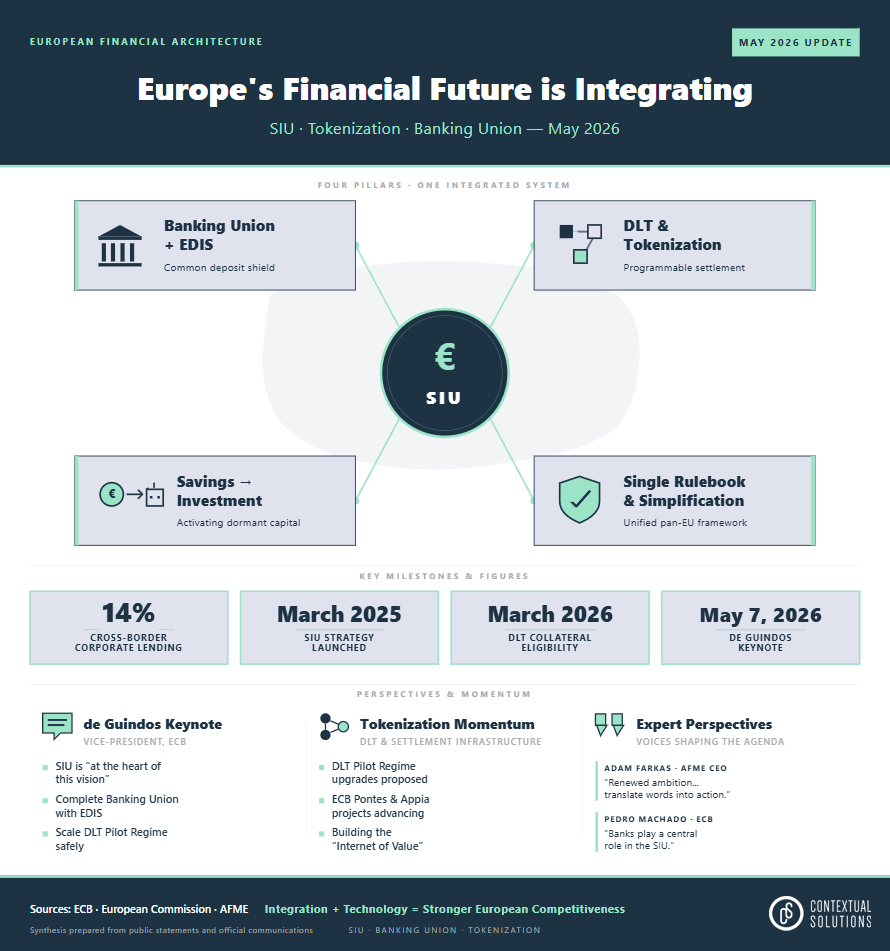

When Luis de Guindos took the podium in Frankfurt on Wednesday, the European Central Bank's vice-president was making a familiar argument with newly urgent stakes. Speaking at a joint European Commission and ECB conference on financial integration, he laid out a vision for a European financial system that has eluded policymakers since the euro's creation. He described a bloc where capital, liquidity, and savings move freely across borders, where banks treat the union as a single jurisdiction rather than a patchwork of twenty national markets, and where new technologies modernize the plumbing of finance without compromising regulatory oversight.

The speech consolidated a project that has gathered momentum over the past fourteen months under the cumbersome but consequential label of the Savings and Investments Union, or SIU. It represents the European Union's most ambitious attempt yet to fix the structural problems that have long left its capital markets shallower than America's, its banks smaller than China's, and its growth slower than either. The question now is whether this iteration will deliver where its predecessors stalled.

An Evolution, or Something More

The SIU emerged from a recognition, articulated bluntly in former ECB president Mario Draghi's report on competitiveness and former Italian prime minister Enrico Letta's report on the single market, that Europe has been quietly losing ground. European households save more than their American counterparts but earn substantially less on those savings. European companies struggle to scale because they cannot access deep equity markets at home, often relisting in New York when they reach a certain size. European banks remain trapped within national perimeters even as global rivals consolidate and digitize.

The European Commission published its SIU strategy on March 19, 2025, branding it as an evolution of the decade-old Capital Markets Union project. Pedro Machado, a member of the ECB's supervisory board, has pushed back against the framing.

"The SIU is often described as a continuation of the capital markets union, but as Commissioner Maria Luís Albuquerque noted, this understates its ambition. The SIU is not designed to crowd-out banks, but to ensure a financial ecosystem in which bank-based and market-based finance support each other."

The new agenda links retail savings, capital markets, banking, and supervision into a single strategic vision rather than a sequence of technical files. De Guindos echoed this expansive framing in Frankfurt, calling the SIU a project that reflects "the essence of the EU project itself: unity, cooperation and shared prosperity."

The Banking Union Problem

De Guindos was sharpest on banking. Despite more than a decade of integration through the Single Supervisory Mechanism and the Single Resolution Mechanism, the banking union remains incomplete in ways that matter for the real economy. Cross-border corporate lending sits at just 14 percent of total euro-area lending, according to fourth-quarter 2025 figures, and equity market integration has actually declined since 2022. Intra-euro-area foreign direct investment is at historical lows.

The missing piece, in the ECB's view, is a European Deposit Insurance Scheme, or EDIS, that would replace national deposit guarantees with a unified backstop. Without it, capital cannot move freely within bank groups, supervisors cannot treat the bloc as a single jurisdiction, and cross-border consolidation remains commercially unattractive. De Guindos was direct about what completion requires:

"The crucial step towards strengthening Europe's competitiveness and deepening financial integration is the completion of a truly single banking market where capital and liquidity can move across borders and all deposits are protected equally."

The language is deliberate, aimed at member states that have spent years resisting EDIS on the grounds that their banks would end up subsidizing weaker neighbors. The argument now being marshalled is that the cost of not finishing the job is mounting visibly in the form of stalled consolidation and shrinking competitiveness.

Tokenization Reaches an Inflection Point

The technological arm of the project is in some ways the more novel terrain. The EU's DLT Pilot Regime, operational since 2023, allows financial firms to test trading and settlement of tokenized securities under modified MiFID II and CSDR rules. Uptake has been disappointing, hampered by an aggregate market value cap of around six billion euros, time-limited permissions, and a general sense that the regime would be superseded before any operator could build a serious business on it.

The Market Integration and Supervision Package proposed by the Commission in December 2025 would address these constraints, lifting the cap to as much as 100 billion euros, expanding the range of eligible instruments, and creating a lighter regime for smaller operators. In April, 39 financial firms reportedly urged regulators to accelerate the upgrades, warning that delay would simply push tokenized capital markets activity to the United States and other jurisdictions willing to move faster. Coen ter Wal, head of technology and operations at the Association for Financial Markets in Europe, framed the stakes in a recent paper on DLT architecture:

"Europe has a real opportunity to leap forward in how its capital markets operate by embracing DLT-based architectures that can overcome the inefficiencies of the current fragmented system."

De Guindos used the speech to endorse the regulatory direction, telling the Frankfurt audience that "by adapting the distributed ledger technology pilot regime, we can facilitate innovation in digital financial services while preserving robust regulatory oversight." The ECB has been working in parallel on the infrastructure side. Its Pontes initiative is exploring the settlement of distributed ledger transactions in central bank money, with pilot elements expected later this year. The Appia roadmap, published in March, sketches a longer-term architecture for an integrated tokenized financial ecosystem grounded in central bank money. From March 30, the Eurosystem began accepting certain DLT-based marketable securities issued through central securities depositories as eligible collateral for credit operations, a concrete step beyond the pilot phase.

From Words to Action

Translation is the hard part. Every meaningful element of the SIU runs through legislative co-decision between the European Parliament and the Council, where national interests reassert themselves with predictable regularity. EDIS has been blocked for years by countries that fear cross-subsidization. Insolvency law, tax, and corporate law remain stubbornly national, creating frictions that no amount of supervisory harmonization can dissolve. Even the technological pillar, which on the surface requires only regulatory adjustments, depends on legal certainty for tokenized assets across borders, interoperability between competing platforms, and the cultivation of secondary market liquidity for instruments that currently exist mostly in pilot form.

Adam Farkas, chief executive of the Association for Financial Markets in Europe, captured the prevailing industry mood when the SIU launched last year:

"AFME has been a strong supporter of the CMU project since its inception in 2015 and we are encouraged to see the renewed ambition of the Commission to pursue and expand the objectives of the CMU through the Savings and Investments Union. It is now for all involved, including EU institutions and Member States, to translate words into transformative action."

What gives the current effort more weight than its predecessors is the geopolitical backdrop. The competitiveness arguments that animated the Draghi report have hardened into something close to consensus across the Commission, the ECB, and major industry groups. Europe is no longer debating whether to integrate but how quickly, and against what alternative scenario. The risk de Guindos described, almost in passing, is that without genuine single-market treatment for banking and capital markets, the bloc will continue to lose share, talent, and capital to jurisdictions that can offer scale and speed. American and Asian financial centers are not waiting for Brussels to harmonize its insolvency regimes.

The next several months will test which version of Europe prevails. Securitisation reforms are working through the legislative pipeline. The 2026 banking competitiveness report is due before year-end. The Pontes pilot is approaching, the Appia roadmap is being filled in, and a private equity exits consultation closes in May. The long-stalled question of EDIS, which has lingered since the original banking union design more than a decade ago, may finally come to a head as part of the broader package. De Guindos's phrase on Wednesday, that "capital follows the real economy," was meant as encouragement. It also reads as a warning. If Europe does not build the financial architecture its real economy needs, the capital, and eventually the economy itself, will simply go elsewhere.